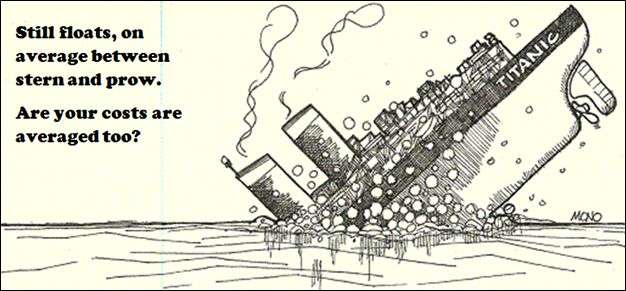

A surface-level answer is simple: divide direct costs by kilogram or by dozen, whichever is your favourite measure of production. Done. Done? Using the resulting number for costing new orders may lead to painful losses. Remember Titanic? With its stern high up and its prow deep low, on average titanic was still floating alright. Using average costs may have the same value.

Let’s take a closer look. Direct cost comprises raw materials, utilities and direct labour. How will these costs change when an industrial bakery switches from Small Bun, weighting 1 kilo per dozen to Big Bun, weighting 2 kilo per dozen?

| 1 kg per dozen | 2 kg per dozen | Proper cost allocation metric | Comment | |

| Raw materials | RM | 2*RM | Kg of product | More product needs more dough |

| Natural gas | NG | 1.5*NG | Kg of product | Oven has higher temp, does not need twice the volume of gas |

| Electricity | El | 1.2*El | Kg of product | Conveyors and ventilation will use almost the same |

| Water | Wa | 1.8*Wa | Kg of product | Recipe water doubles, cleaning is the same |

| Direct labour | DL | DL | Number of pieces of product (number of packages) |

Size of bun makes no difference |

(Though numbers in this table do not represent any particular bakery or product, they are common.)

We see now that allocating direct costs neither by kilogram, nor by dozen, will result in correct product cost: allocating costs of raw material and utilities per kilogram and costs of direct labour per package will be much closer to what bakery really spends, than choosing either of these metrics for all cost categories. And by ‘correct’ here I do not mean ‘meeting accounting rules’ or ‘following corporate procedures’, ‘correct’ here stands for bottom line: doing differently will cause lost profit up to selling below actual cost.

Proper analysis of actual costs will allow empower production manager to achieve fair profit margin while talking with CFO or with client.

Leave A Comment