The business value of an energy management project commonly exceeds direct savings. Aside from this fact, do most managers actually know the amount of direct savings achieved through their energy management projects? A recent report produced by The Ethical Corporation, UK offers a comprehensive picture of how organizations around the world are approaching sustainability. This research report, titled State of Sustainability 2015, clearly demonstrates a gap between reported savings and confidence in these same numbers.

Who believes reports about savings from sustainability projects?

This is a peculiar observation by itself, yet the situation gets even more peculiar. Responses from reporting managers and from decision-makers (C-level/Executive/Board) are averaged in this research. Naturally, those who measure have higher trust than those who read report about measurement. Therefore, senior decision-makers likely have much less trust in savings resulting from sustainability projects than reporting managers. Lower trust creates higher hurdles and decreases the number of sustainability projects approved.

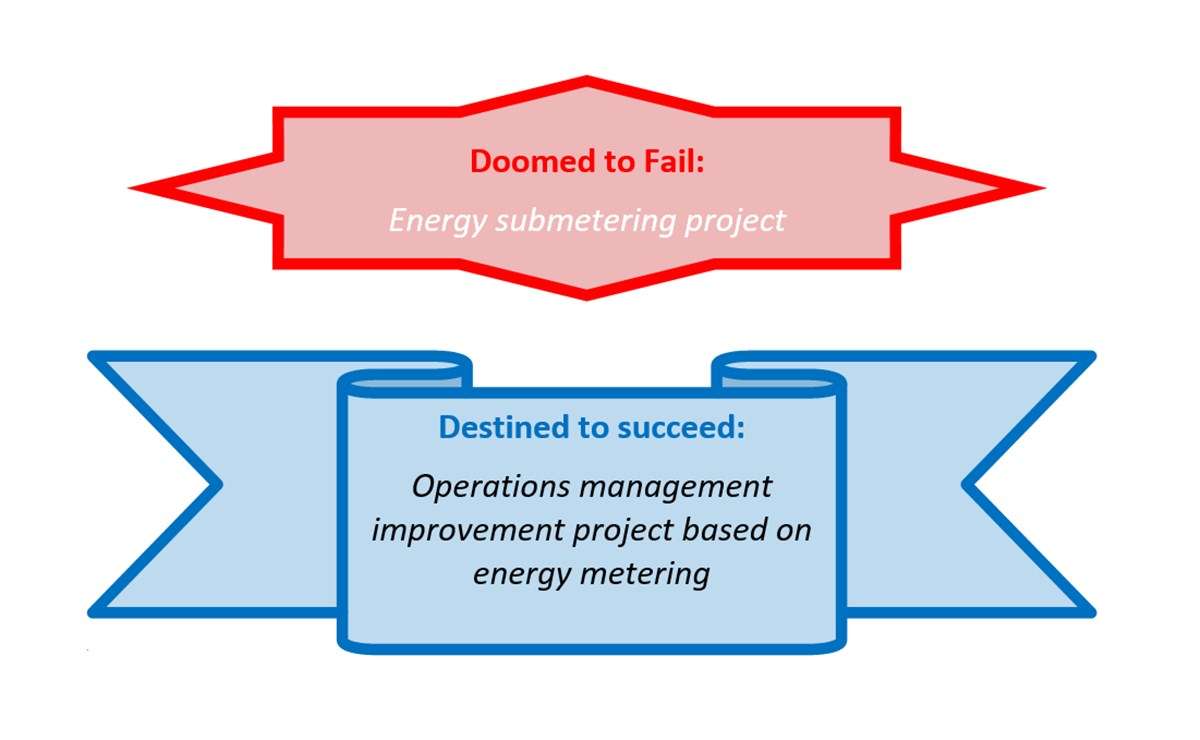

Tracking direct savings with respect to bills is rarely an easy job. Estimating the indirect business value of energy management projects is even more difficult: for example, an efficient baking oven works at optimal temperature thus assuring that bread has consistent quality, what is the monetary value of this?

How do we convince senior decision-makers that energy management is profitable?

Measuring savings is not an easy job because the operational conditions change all the time. Comparing consumption “Monday to Monday” or “June to June” is often meaningless. Therefore energy managers commonly rely on calculations produced by equipment vendors. Well, this is akin asking a vendor if their equipment is good, right? Decision-makers indeed understand this and discount results mercilessly. It’s hard to blame them.

Convincing senior leaders that sustainability projects achieve results is another significant challenge, but it can be done. The following activities can help to increase trust in reported results and secure funding for energy management initiatives:

- Measure—collect data on energy consumption consistently, in a way that permits further analysis.

- Analyze—identify clear relationships between core activities and energy consumption.

- Report—demonstrate savings by comparing baseline consumption (business as usual) with actual consumption after implementation of energy efficiency measures.

- Act—identify the root causes of unexpected overuse (e.g., waste, higher need from operations), and identify the financial cost of operational changes.

- Present—convert information about savings achieved into operational numbers that decision-makers can understand. For example, reporting might explain that “savings from energy efficiency delivered gross profits equivalent to those resulting from shipment of XX tons of product”. Reporting could also express savings in terms of equivalent days of operation, or an increase in profitability or occupancy.

Done right, these steps assure consistency in evaluation of efficiency projects, make reported results relevant and trustworthy to C-level managers.

Leave A Comment